The movie, The Big Short, has already been nominated for four Golden Globe awards and it will certainly win an Academy Award or two.

But how accurate is The Big Short? Did it correctly lay out the root causes of the Great Housing Bubble and the Great Recession or did the movie take a lot of poetic economic license?

To find out, I interviewed Anthony Sanders, Distinguished Professor of Finance in the School of Management at George Mason University. He previously taught at University of Chicago (Graduate School of Business) and The Ohio State University (Fisher College of Business). He served as Director and Head of Asset-backed and Mortgage-backed Securities Research at Deutsche Bank in New York City.

Dr. Sanders has a blog popular among economists and real estate geeks called “Confounded Interest”.

Dr. Sanders discusses the reasons given in the movie, The Big Short, and other popular explanations for the Great Real Estate Bubble.

- Mortgage backed securities and collateral debt obligations

- Corruption at the bond rating agencies

- Regulators who were too close to the banks

- Fed interest rate policy

- Repeal of the Glass Steagall Act

Dr. Sanders explains what really caused the Great Real Estate Bubble and the Great Recession.

More from Dr. Sanders

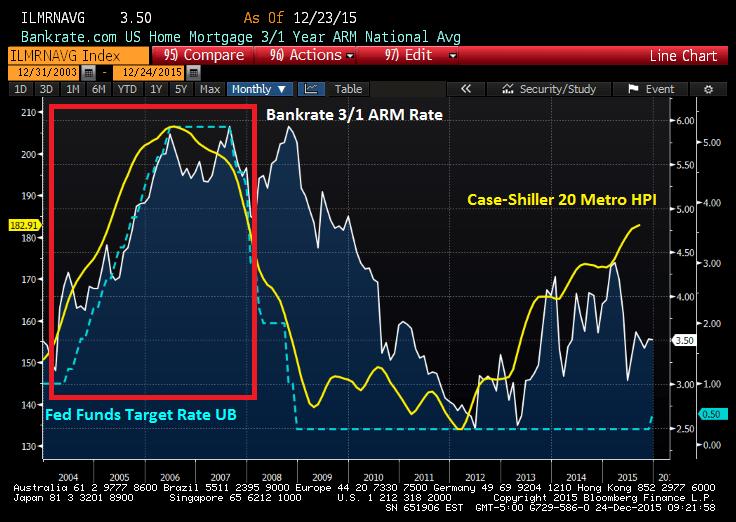

What “The Big Short” Left Out in One Picture (Hint: The Federal Reserve and ARMs)

“Back in June 2004, The Federal Reserve began to frantically raise the Fed Funds Target Rate from 1% until it peaked in June 2006 at 5.25%… Hence, the 3/1 ARM rate rose from 3.15% in March 2004 to 5.84% in June 2006, a 270 basis point increase.”

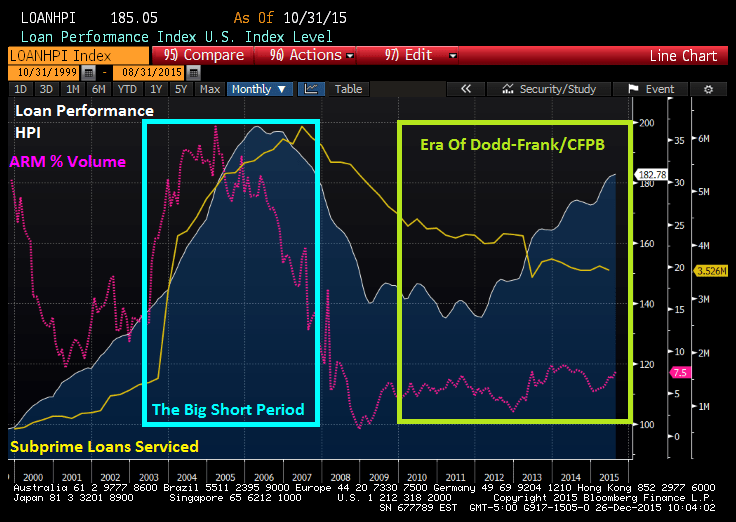

The Big Short and the Era of Regulation (Dodd-Frank and Consumer “Protection”)

“Essentially, banks (under control of The Federal Reserve) can no longer originate subprime loans to consumers… Banks can no longer originate exotic ARMs like pick-a-pay or NINJA (no income, no job) loans. Lenders must now show that the borrower has the ability to repay the loan (rather than just saying ‘Yup, I sure can!’).”

Paramount’s “The Big Short” in Pictures: Lehman, Bear, and Credit Default Swaps (CDS)

National Homeownership Strategy

Note from John. The homeownership rate in the U.S. fell 1 percentage point from 64.7% when the National Homeownership Strategy was adopted in 1995 to 63.7% today. Worst of all, the volatility of home values absolutely skyrocketed. By blindly promoting homeownership, they destroyed a lot of wealth, especially among low income homeowners. The goal should have been maximizing long-term wealth creation among low and moderate income families, not maximizing homeownership at all costs.

I don’t see how the National Homeownership Strategy could have been a bigger failure.

###

5 Responses to How Accurate is "The Big Short" Movie Economically?

[…] #5 – How Accurate is “The Big Short” Movie Economically? […]

[…] at http://www.realestatedecoded.com/how-accurate-is-the-big-short-movie-economically/ […]

Just watched the Big Short movie earlier this week (finally arrived at the top of my Netflix). I like this interview with Anthony, nice job including the charts within the interview — makes the subject tangible, like the movie did.

That’s a good final point too John about National Homeownership Strategy.

Allow me to be cynical because I’m working on the ground handling home sales and purchases daily — think a lot of FHA buyers (who put only 5% cash down) want to buy their home not because they need a place to live (there are already an abundant number of affordable places to rent). I think FHA buyers primarily want to buy because they are hedging their bets — they have housing fever and want to roll the dice for profits. When the next default comes, I’m sorry, but I won’t see these FHA buyers as victims anymore than the guy at the blackjack table in Las Vegas is a victim — he got a free drink for sitting down at the table for five minutes. If he loses, he’ll make a stink face, but it’s his own risk. Sadly, the FHA process puts his risk on the populace, which I think is bad policy. Why would they set national policy on 5% cash down?

As Anthony quoted another during the interview, “This is a new economy, risk doesn’t matter.”

So, when is the next big default coming?? Or when will median household income drop while home prices continue to rise in an environment of easy subprime credit?

Great comment as always!

When they make loans to under-qualified borrowers, FHA hurts poor neighborhoods because they increase the number of foreclosures in poor neighborhoods.

Good point John.

I have a news development on the ground here in the California real estate market — subprime credit in 2016 is even worse than it was in 2009. An example from this month:

It’s May 2016 and I just saw something new in Oakland, CA – a conventional loan preapproval letter for only 3% down!! The buyer does not even have enough cash reserves to cover the closing costs (so they need a Seller credit on that item), but the buyer is still approved for a home worth over 1/2 million dollars at only 3% down. Unbelievable!

Get ready for the next Big Short…

Comments are closed.