When I take home buyers into a house for the first time, it seems they’re all reading from the same script, “What’s the price? How long’s it been on the market?”

How home buyers think. You see what buyers are doing there with the second question, “How long’s it been on the market?” They’re trying to estimate how overpriced the house is. The longer it’s been on the market, the more overpriced buyers think it is. It could have had a large price reduction yesterday but buyers will still key on how long the home has been for sale.

What’s the real price? Buyers know that sellers almost alway overprice their homes. So whenever a buyer sees a price, they immediately start estimating the seller’s bottom line price and if it’s close enough to the buyer’s idea of fair market value for the house, they might make an offer.

The biggest clues buyers use for determining the seller’s bottom line price are the list price, of course, and how long the house has been on the market. The buyer is asking, “If I make an offer, will I be able to negotiate the price down to a good price?”

Negotiating leverage. The buyer’s negotiating leverage grows the longer the home has been on the market. Real estate agents see this all the time. Sellers who are strident about their price and say, “I’m not going to give it away” slowly, as the home stays on the market unsold, may reevaluate the home’s value and lower the list price.

Here’s the puzzle. Pricing homes is a HUGE issue and it’s an especially interesting issue for a former economist like me. Economists love pricing questions.

Goal. I wanted to see how negotiating leverage changes between buyers and sellers as time on market increases for homes listed for sale.

Let’s check it out!

Negotiating Leverage and Days on Market

When a home is on the market for a long time without selling two things often happen, 1) the seller lowers the list price, and 2) buyers are able to negotiate more off the list price.

I’m going to look at 2) in this post and 1) in a future post.

Negotiated price reductions. I compared the final list price to the sold price of all single family detached homes sold via the metro Phoenix MLS (where I have access to the raw data) in 2014 that were not foreclosures or short sales. I only looked at homes that actually sold in 2014. I didn’t look at home that were listed for sale but failed to sell in 2014. The dataset had 57,702 home sales.

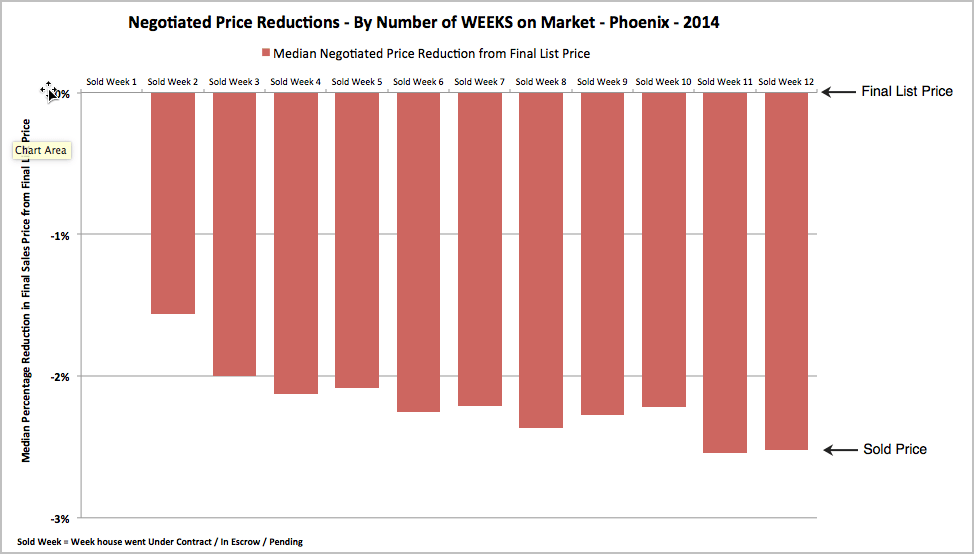

Typical Negotiated Price Reductions – First 12 Weeks

English explanation. The top line of a bar – the 0.0% line – represents the list price when homes went under contract. The red bars represent the median, or typical, amount the price was reduced in the final sales price.

Geeky explanation. I took all the homes that sold the first 7 days on the market (10,893 homes), for example, calculated the difference between the final list price and the actual sold price for each of those 10,893 sales and then calculated the median which is the typical negotiated price reduction for homes that sold that week.

I’m using the term “sold weeks” to mean the number of weeks from the time the house first hit the market (hit the MLS) to the time the house went under contract to the actual buyer.

1st Week Sale Typically Means Full List Price

The most amazing thing on this graph is that the typical home that sold the 1st week it was on the market sold for full list price. More precisely, half the homes that sold the 1st week on the market sold for full list price or more, and half sold for full list price or less.

This large “1st week effect” that favors sellers by about 2% of the home’s value is mostly gone by the 2nd week and is completely gone by the 3rd week. What’s happening?

Fear of loss. I think the 1st week effect is clearly caused by fear of loss.

I had some clients who were very picky. We looked at a ton of homes. One time I thought we had found “The One.” The decision maker was the wife and she really liked the home.

Her: “I can see myself living here. The price is good. How long’s it been on the market?”

Me: “4 months.”

Her: “Hmm. Let’s keep looking. Maybe we can find something even better. We can always come back to this house.”

Me (thinking): Arghh!

If it had been on the market 4 days instead of 4 months she would jumped at it and been afraid of losing the house to another buyer. She would have considered herself lucky to snag it at full list price.

Fear of loss explains why the typical house that goes under contract the 1st week on the market sells for full list price.

Fear fades fast. Another amazing thing is how fast sellers lost their negotiating advantage. If a house went under contract the 2nd week, the price was typically 1.6% lower than if it had sold the 1st week. If it went under contract the 3rd week, the price was 2.0% lower.

Fear to greed. After the 2nd week it looks like fear of loss is gone and a different mechanism kicks in for the duration. It seems buyers’ focus changes from fear of losing the house to trying to get the lowest price for the house.

It’s not huge but… The seller’s negotiating leverage fell about 0.058% per week from the 3rd week to the 12th week. That means that for a $200,000 house, the sellers negotiating leverage fell about $116 per week or a total of about $1,000 from week 3 to 12. That’s not huge but I think a bigger impact of time-on-market is on how low the list price needs to be before a buyer will even make an offer… but that’s a topic for another post.

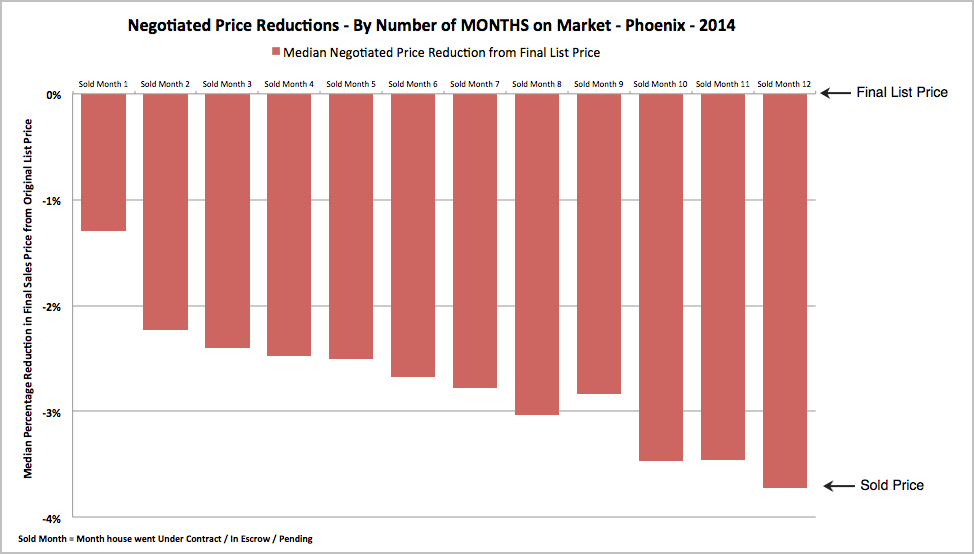

Typical Negotiated Price Reductions – First 12 Months

This 12-month chart shows you how the negotiating leverage continues to weaken for home sellers as time goes on but please be aware that not a lot of homes are sold in the out months.

Of homes that actually sold in 2014, half were under contract by their 5th week on the market and more homes were sold their 1st week on the market than any other week.

Tips for sellers. When homes are too overpriced, buyers don’t make offers. Some sellers say, “I just want to try pricing it high because buyers can always make an offer.”

“Let’s just try this price.” The truth is the typical buyer won’t make offers on homes they think are too overpriced. The typical buyer makes a snap judgement about the seller’s personality and whether they’d be able to reach an agreement with the seller on price. If the buyer can’t visualize the seller lowering the price enough, the buyer moves on.

Opportunity cost. And while a buyer is negotiating with a seller who won’t come down to fair market value, the buyer could lose a great, well priced home that just hit the market. Remember, in a normal market about 30% of the listings you see online won’t sell because they’re too overpriced. Buyers don’t make offers on homes they think are too overpriced.

2% Overpricing Rule

Buyers seem comfortable making offers on homes they think are 2% overpriced. As overpricing increases, buyers are less likely to make an offer.

- You’re most likely to get a premium price for your home if it sells the 1st week on the market.

- The typical buyer is comfortable making offers on homes that are up to 2% overpriced.

- To improve the odds of getting a premium price offer for your home, don’t list it for more than 2% above its fair market value.

- The hard part is figuring out fair market value.

Here’s the problem. We’re human. We naturally overestimate the value of stuff we own.

The average American thinks their home is worth 8% more than it is, so when you add 2% to that you’re overpriced by 10% and, therefore, very likely to end up among the 30% of listings that fail to sell.

Caveat: The data came from home sales in metro Phoenix AZ in 2014 which was a more or less normal year, the real estate market wasn’t really hot or cold. The numbers would likely be different in hot or cold real estate markets.

# # #

See all “How to Price Your Home” posts here.

A Few Related Academic Articles

Economist have often looked at how prices are determined for homes and they usually use a theoretical framework called Search and Matching Theory. They compare finding a home to finding a job. I don’t think it works well. It certainly doesn’t work well today when information about homes for sale diffuses amazingly fast with the help of the internet. I think the home selling process is a lot more like a string of auctions with declining attendance from bidders than a job search.

- Market Thinness, List Price Revisions and Time to Sell: Evidence from a large-scale housing dataset

- Liquidating Real Estate Assets Quickly: What Affects the Probability of a Quick Sale?

- Listing Price, Time on Market, and Ultimate Selling Price: Causes and Effects of Listing Price Changes

- House Prices, Sales, and Time on the Market: A Search-Theoretic Framework

- The Trade-off Between the Selling Price of Residential Properties and the Time-on-the-Market: The Impact of Price Setting

- List Prices, Sale Prices, and Marketing Time: An Application to U.S. Housing Markets

3 Responses to Price Your Home to Sell Fast & For Top Dollar

I read a story from a real estate agent in a Facebook group yesterday about making a reasonable offer on an overpriced home. The agent was very frustrated that the seller (also an agent) rejected her clients’ offer but wouldn’t send her any comps justifying the list price.

And that reminds me of what I like to tell my buyer clients, “Don’t assume the seller is rational.” “We’ll find out if they’re reasonable sellers or crazy sellers by how they react to your offer. About 30% of listings fail to sell because a lot of sellers aren’t rational.”

If your house doesn’t sell at the price you need, at what point should you take it off the market and reconsider? If you loose your negotiating after 3-4 weeks, what the point of keeping it on the market?

Most homes that sell after being on the market 3-4 weeks have had at least one price cut and then the buyer negotiates the actual sale price down from there (typically negotiated down another ~2% from the final list price in Phoenix in 2014).

FYI, in Phoenix in 2014, half the homes that ended up actually selling were under contract within 5 weeks of hitting the market. If your home is on the market more than 5 weeks, you’re not doing as well as the typical successful seller.

If you can’t lower the price anymore – like I think you’re saying – that’s a bad situation to be in. The house could still sell at the price you need in the future but time is against you. It’s more common that the seller has to reduce the price to get an offer and the total cumulative price reduction has to be larger the longer the home is on the market.

If you have other options (renting it out, not moving) consider them early so if the house isn’t getting interest so you don’t waste months with it on the market slowly losing value.

I’d say ideally you need to reconsider the price every 3 weeks, every 4 weeks at the most. After 6 to 8 weeks, if you really can’t lower the price anymore, that’s when you get serious about reviewing your options to take it off the market and look at Plan B.

If you put the home on the market during a slow time of year, you’d want to extend those times.

Wow, that was long and I’m not even sure I answered your question. 🙂

Ask it another way if I didn’t answer your questions.

Thanks!

Comments are closed.