Here’s a different way to look at mortgage interest rate declines.

The 30-year fixed-rate mortgage interest rate fell from 4.94% in November 2018 to 2.65% in January 2021. That decline was so large, we could have changed the standard U.S. mortgage from 30 years long to 20 years long without increasing monthly principal and interest mortgage payments!

In a little over 2 years, we could have gone back to 20-year mortgages like we had during the post-World War II housing boom.

When mortgage rates fall, three things can happen, 1) monthly mortgage payments can fall, or 2) the amount borrowed can increase, or some of both. But there’s a third option that’s rarely talked about. When interest rates fall, 3) the length of mortgages can be shortened.

3 Potential Impacts Of Lower Mortgage Interest Rates

(Click graph for interactive version.)

In reality, when rates fell from late 2018 to early 2021, the lower mortgage rates let house buyers borrow a lot more money with the same monthly mortgage payments. (See graph below.) It doesn’t take a whole lot of aggressive buyers – who can now borrow a lot more money – to bid up house prices for everyone.

If Lower Rates Went Entirely To Borrowing More Money

(Click graph for interactive version.)

As mortgage interest rates fall, the amount of money chasing houses increases. But as house prices increase, monthly mortgage payments also increase.

Monthly payments can end up increasing back to where they started from before mortgage rates fell. If house prices gain a lot of upward momentum, they can overshoot on the upside and monthly payments can end up going even higher than they were before mortgage rates started to fall.

That’s where we are now in most of the United States – mortgage rates fell off a cliff and then house prices skyrocketed. Nationally, most of the advantage of falling mortgage interest rates since November 2018 had already been offset by higher house prices by January 2021.

If house prices continue rising extremely fast as expected, the advantages of the lower mortgage interest rates since 2018 will be completely gone, completely offset by higher house prices. The mortgage payment price of U.S. houses will soon be back to where they were in November 2018 despite the lower mortgage rates.

The benefits to home buyers of lower mortgage interest rates are short-lived. The resulting higher home prices are long-lived.

The U.S. mortgage system is not set up for this but, theoretically, here’s what it would look like if lower mortgage interest rates could somehow be converted into shorter standard mortgages instead of larger mortgages and then higher house prices.

- In November 2018, a $2,000 per month mortgage principal and interest payment for 30 years at 4.94% interest would qualify you to borrow $375,000.

- In January 2021, a $2,000 per month mortgage principal and interest payment for 30 years at 2.65% interest would qualify you to borrow $495,000.

- In January 2021, a $2,000 per month mortgage principal and interest payment for 20 years at 2.40% interest would qualify you to borrow $380,000. (20-year mortgage rates run about 0.25% less than 30-year mortgage rates.)

Notice, due to the lower mortgage interest rates – with the same monthly payment – you could borrow the same amount in January 2021 with a 20-year mortgage as you could in November 2018 with a 30-year mortgage.

In this alternate mortgage universe, instead of letting lower mortgage interest rates drive up house prices for all future house buyers, we could have theoretically shortened mortgages by 10 years for all future house buyers – without increasing monthly mortgage payments.

Winners & Losers In This Alt-Universe Where 20-Year Mortgages Become Standard

First-time house-buyers would be the big winners in this 20-year mortgage universe. House prices would be lower than with 30-year mortgages, and home buyers would have 120 fewer mortgage payments to make. They would pay far less money to the financial sector in interest over the life of their mortgages which means they could save more for retirement. They would be far more likely to own their houses free and clear before they retire. This group would include a lot of Millennials, most Gen-Z, and all future generations.

In addition, 20-year mortgages have MUCH lower foreclosure rates than 30-year mortgages, in part, because your equity grows so much faster. You’ll have paid off 10% of the principal of a 20-year mortgage (at 2.40% mortgage interest rate) after 2.5 years but with a 30-year mortgage, it would take you over 4 years to pay off 10% of the principal (at 2.65% mortgage interest rate). After 20 years, you’ll have paid off 100% of the 20-year mortgage, of course, but only 56% of the principal of the 30-year mortgage. Faster wealth creation means fewer foreclosures when things go south, and that means more stable families financially and otherwise.

Current homeowners who have mortgages with less than 20 years left, would benefit from refinancing into lower interest rate mortgages like they did in reality. Homeowners with more than 20 years left on their 30-year mortgages, would benefit from refinancing into shorter, 20-year mortgages with the same and/or lower monthly payments. Overall, household debt would begin falling.

Current homeowners, however, would not see their house prices increase by nearly as much. Lower mortgage rates would be converted into shorter mortgages instead of larger mortgages and then higher house prices. Boomer and Gen-X homeowner net worth wouldn’t increase as much in this universe but stronger, more stable economic growth would greatly benefit everyone, including homeowning Boomers and Gen-Xers.

Real estate agents overall would be worse off. For example, the median U.S. house price has already increased more than $50,000 since interest rates started falling in November 2018. If we assume 5 million home sales per year and real estate agents make 5% in commissions on each sale, that $50,000 price increase means $2,500 in additional real estate agent commission income per house sold, or $125 billion in additional real estate agent commissions – per year – every year – due to the house price increases caused by the falling mortgage interest rates since late 2018. And house prices are going to continue to increase for many months due to the mortgage rate decreases in 2019 and 2020.

The mortgage industry would be worse off to the degree they make less money on smaller mortgages. The falling mortgage rates would still lead to a huge refinancing boom but house prices wouldn’t have increased as much in this scenario where 20-year mortgages become standard. Overall, mortgage debt and mortgage industry revenue and margins would increase less.

The financial sector would be worse off. They make a lot less money on shorter mortgages. Let’s look at the mortgages outlined above in a different way.

- In the second example above, the total interest paid to the financial sector over the life of a 30-year mortgage for $495,000 at 2.65% interest would be $220,000.

- In the third example above, the total interest paid to the financial sector over the life of a 20-year mortgage for $380,000 at 2.40% interest would be $100,000.

U.S. Economic Growth Would Be The Other Big Winner

Economic growth. Lower house prices and less money chasing homes due to shorter mortgages would mean less money wasted on paying interest to the financial sector. Overall, homeowners would have more money to spend in the productive, job-creating economy, every year, year after year.

Economic stability. Shorter mortgages would reduce the size of real estate booms and busts which would increase overall economic growth over the real estate cycle, all other things being equal. With more people owning their houses free and clear, consumer spending would fall less in recessions, and recessions would be smaller and shorter.

Having less mortgage debt is especially important when house prices fall. Falling house prices can create a negative feedback loop where falling prices create foreclosures which create more falling prices, and more foreclosure, and so on. When homeowners have more home equity, it always slows down and could sometimes prevent that downward price spiral.

More stable household wealth creation. Fewer and smaller real estate booms and busts would greatly stabilize family wealth creation. Families would lose a lot less wealth during the fewer, smaller, and shorter real estate downturns.

Wealth equality. The current system converts lower interest rates into higher house prices, which creates wealth for current homeowners but, in the long run, hurts younger families that don’t already own houses. Converting lower interest rates into shorter mortgages helps all future homeowners to reliably build family wealth faster.

Stock market. Investing in real estate competes with investing in the stock market. If houses appreciate less (when interest rates fall), then investing in the stock market becomes a relatively better investment because the stock market increases when interest rates fall. More money would flow into the stock market and into other investments that create a LOT more jobs per dollar invested than mortgages.

Instead of depending so much on house price appreciation for wealth creation like for the Baby Boomers, home buyers in this scenario would be able to create wealth reliably by paying off their mortgages 10 years earlier. That would let them spend, save and invest a lot more which would be great for economic growth in the United States. They would save a lot more for retirement after they pay off their mortgage which would also benefit parts of Wall Street.

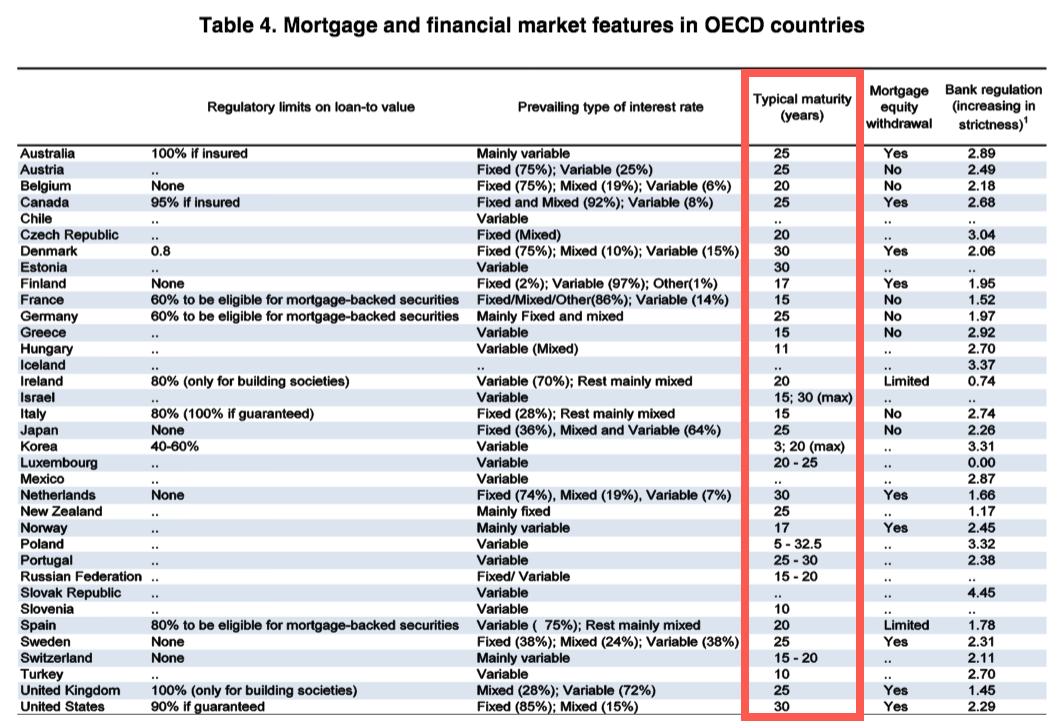

30-Year vs. 20-Year Mortgages Internationally

I quipped that converting lower interest rates into shorter mortgages would only happen in an alternate universe but 20-year mortgages are actually very common in other countries.

One study found that in only 23% of the countries studied was the typical mortgage 30 years long. In nearly half of the 31 countries studied, the typical mortgage was 20 years or LESS.

Although U.S. real estate trade associations act like the 30-year mortgage was handed down from Mount Sinai, mortgages are typically much shorter around the world.

Typical Length (term/maturity) Of Mortgages In OECD Countries

Source: Andrews, D., A. Caldera Sánchez and Å. Johansson (2011), “Housing Markets and Structural Policies in OECD Countries”, OECD Economics Department WorkingPapers, No. 836, OECD Publishing, (Page 33). Graphic annotated by John Wake.

[That next-to-last column in the graphic is also fascinating! It looks like many countries restrict house equity withdrawal, for example, by restricting second mortgages, cash-out refinancing, and/or, home equity lines of credit.]

[It’s very hard to find economic studies that compare mortgage design and real estate regulation internationally. Why doesn’t some university have an center for “Comparative Economics of Mortgage Design and Real Estate Market Regulation”?]

Conclusion

This article is a thought experiment in economic science. Political science will likely prevent any changes to the status quo 30-year mortgage in the United States even though shorter mortgages would lead to larger, more stable economic growth nationally, as well as larger, more stable, and more equal family wealth.

Thesis. Instead of having lower mortgage interest rates being converted into higher house prices, we could have theoretically shortened mortgages when rates fell – without increasing mortgage payments – and, in addition, that would have prevented the lower interest rates from being converted into higher house prices. Both effects would be big wins for all future U.S. home buyers and the U.S. economy.

At least, I hope this thought experiment helps you see how huge the mortgage interest rate declines from November 2018 to January 2021 were, and how they could cause the huge increases in house prices we’ve seen and continue to see.